· 4 min read

Income Needed for a $300,000 House in 2026

The income needed for a $300,000 house in 2026 depends on your DTI ratio, interest rate, and loan type. See real payment examples.

Quick Answer

- With no other debt, you need roughly $98,000 per year in gross income to afford a $300,000 house in 2026.

- With moderate existing debt (car payment + student loans), required income drops to about $83,000–$90,000 per year using a 43% back-end DTI.

- FHA loans can lower the threshold to approximately $71,000 per year, though mortgage insurance premiums apply.

- Your exact requirement depends on interest rate, down payment, property taxes, and credit profile.

The income needed for a $300,000 house in 2026 depends on your debt-to-income (DTI) ratio, interest rate, and total monthly obligations.

This guide breaks down the income required for a $300,000 home in 2026 using realistic numbers and lender standards.

Step 1: Estimate the Monthly Mortgage Payment

Assumptions for this example:

- Home Price: $300,000

- Down Payment: 10% ($30,000)

- Loan Amount: $270,000

- Interest Rate: 6.5%

- Loan Term: 30 years

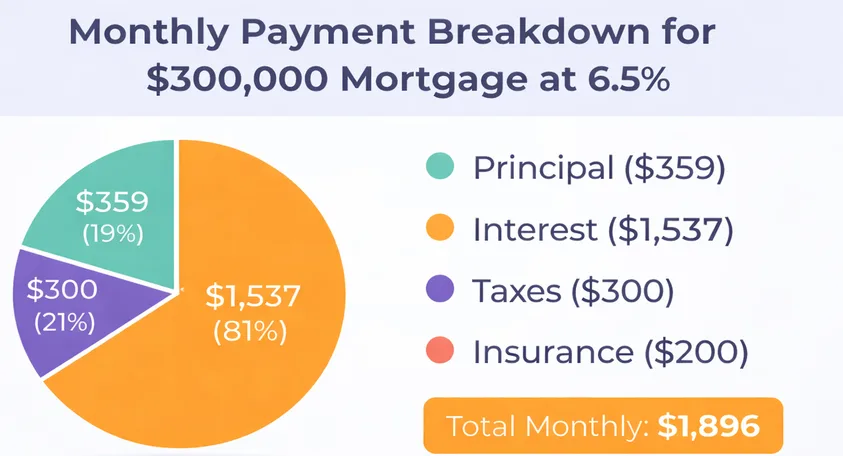

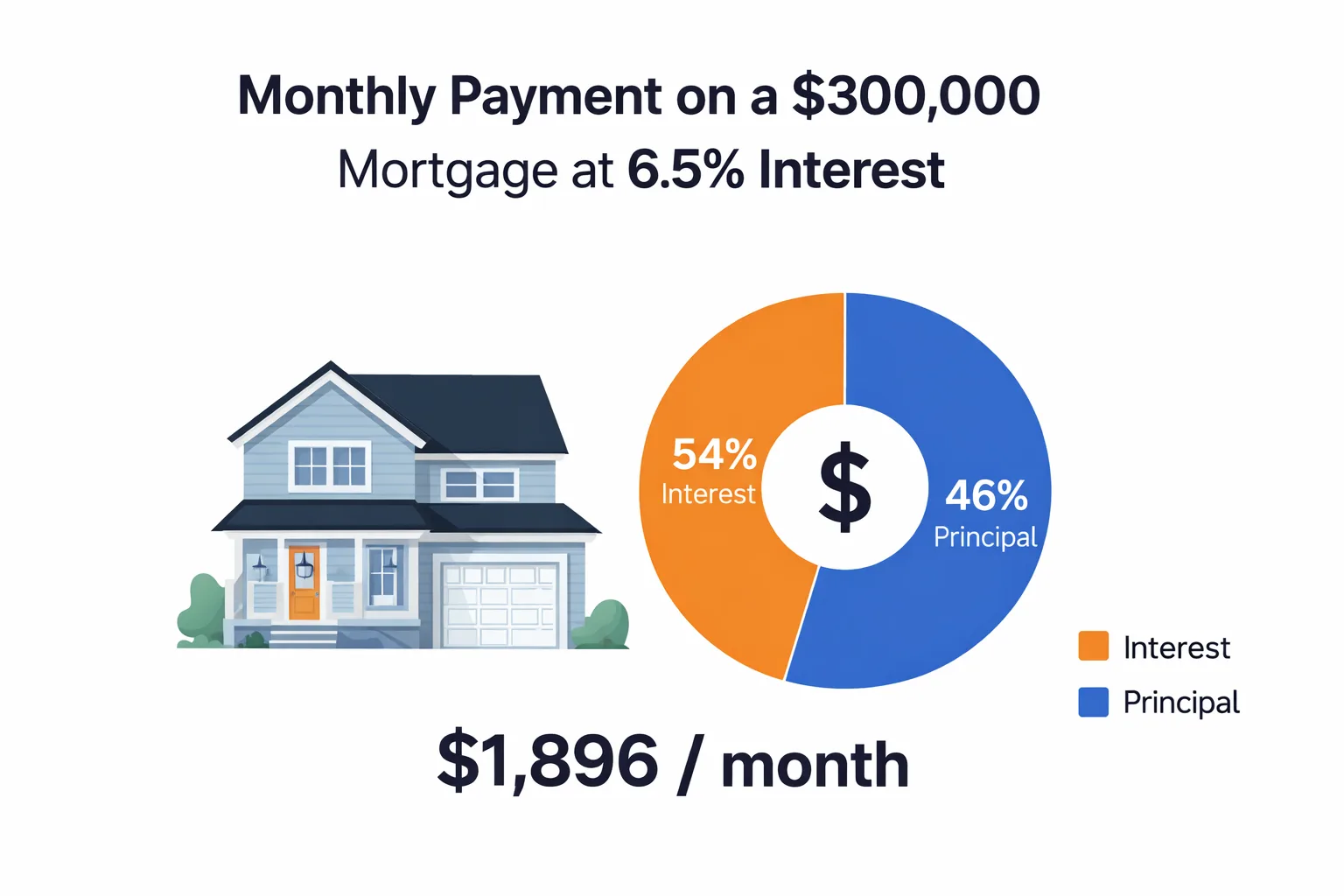

Estimated Principal & Interest: approximately $1,707 per month

Now add typical costs:

- Property Taxes: $300

- Home Insurance: $150

- PMI (if applicable): $120

Estimated Total Monthly Payment: approximately $2,277

This may vary by state. Use our Mortgage Calculator for exact numbers.

Step 2: Understand Debt-to-Income Ratio (DTI)

Lenders typically allow:

- 28%–31% of income for housing (Front-End DTI)

- 36%–43% total debt (Back-End DTI)

Most conventional loans allow up to 43% DTI.

DTI Formula:

Total Monthly Debt Payments divided by Gross Monthly Income equals DTI percentage.

Step 3: Calculate Required Income (No Other Debt)

If your housing cost is $2,277 per month and you have no other debt:

To stay under 28% front-end DTI:

$2,277 divided by 0.28 = $8,132 gross monthly income

That equals approximately $97,584 per year.

So if you have no other debt, you would need about $98,000 annual income to comfortably qualify.

Step 4: Example With Other Debts

If you also have:

- Car payment: $400

- Student loans: $300

Total Monthly Debt = $2,277 + $700 = $2,977

Using a 43% back-end DTI:

$2,977 divided by 0.43 = $6,925 gross monthly income

Approximately $83,100 per year.

So depending on debt and loan type, required income could range from $83,000 – $100,000 annually.

FHA Loan Scenario

FHA loans allow higher DTI (sometimes up to 50%).

Using 50% DTI:

$2,977 divided by 0.50 = $5,954 monthly income

Approximately $71,448 per year.

However, FHA includes mortgage insurance premiums, which increase monthly costs.

Factors That Change the Income Requirement

- Interest rate changes

- Property taxes (state-dependent)

- HOA fees

- Down payment size

- Credit score

- Loan program (FHA, VA, Conventional)

Quick Summary

To afford a $300,000 house in 2026:

- With no debt: Around $98,000 income

- With moderate debt: $83,000–$90,000 income

- FHA flexibility: As low as $71,000 (depending on approval)

Assumptions

- Home price: $300,000

- Down payment: 10% ($30,000), resulting in a $270,000 loan

- Interest rate: 6.5% fixed, 30-year term

- Estimated principal and interest: $1,707/month

- Property taxes: $300/month; home insurance: $150/month; PMI: $120/month

- Front-end DTI threshold: 28%; back-end DTI threshold: 43% (conventional) or 50% (FHA)

- Other debt example: $400 car payment + $300 student loan = $700/month

Frequently Asked Questions

Q: Can I buy a $300,000 house making $75,000 per year?

A: Possibly, with low debt and FHA approval, but approval may be tight depending on local property taxes, insurance costs, and your existing debt obligations. Running a detailed calculation for your situation is recommended.

Q: Does down payment change income requirements?

A: Yes. A larger down payment lowers your loan amount and monthly payment, which reduces the income required to meet lender DTI thresholds. A 20% down payment also eliminates the need for PMI.

Q: What credit score do I need to buy a $300,000 house?

A: Conventional loans typically require a credit score of 620 or higher. FHA loans may allow scores as low as 580 with a 3.5% down payment. Higher credit scores generally unlock lower interest rates.

Q: What is a debt-to-income ratio and why does it matter?

A: Your DTI ratio compares your total monthly debt payments to your gross monthly income. Lenders use it to assess risk. A lower DTI makes it easier to qualify for a mortgage and may help you secure better loan terms.

Q: How does interest rate affect the income I need?

A: A higher interest rate increases your monthly payment, which raises the income you need to meet DTI requirements. For example, at 7% instead of 6.5%, your monthly payment on a $270,000 loan increases by about $90, requiring roughly $3,800 more in annual income to qualify under the same DTI rules.

Use our Mortgage Calculator to estimate your exact payment based on your numbers. Understanding your DTI and income requirements helps you shop confidently and avoid surprises during pre-approval.